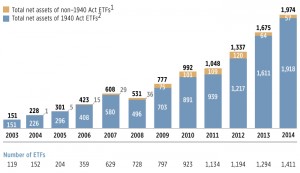

Exchange Traded Funds (ETFs) are among the fastest growing investments in the US. Often described as “mutual funds that trade like stocks”, ten years ago there were barely 200 ETFs with a total of $300 million Today there are over 1,400 ETFs holding ~$2 trillion dollars covering a dizzying array of categories and niche strategies.

Are ETFs right for you? NN provides thoughts on that below:

- Low cost: ETFs are generally viewed as having lower expenses than mutual funds. While this is true, it may be an apples to oranges comparison. ETFs are primarily run as index funds, meaning the idea is to match the performance of a certain area of the market. On the other hand, most mutual funds are run by people making decisions with the goal of outperforming a particular market.segment. When the costs of an (index) ETF are compared with those of an (indexed) mutual fund, expenses are about the same. One other consideration is that investors incur a trading fee/commission with (most) ETF transactions. Meanwhile most mutual funds are now offered commission/transaction free (but as NNs has warned, watch out for that backend load/transaction fee).

- Liquidity: ETFs trade all day long like stocks. Mutual funds trade only at the end of the day. One can instantly determine the price of an ETF, and create a transaction, while a mutual fund investor has to wait until the end of the day. A key caveat is that some ETFs are thinly traded. This can result in a larger “bid-ask” spread where a gap exists between the value of the ETF’s underlying securities and its current market price. Such discrepancies are typically short-lived and fairly small. Nevertheless mutual funds argue that being priced after the market closes ensures the investor receives a fair price as determined by the final day prices of its underlying securities.

- Tax Efficiency: Mutual funds create the potential for “pass through” capital gains tax liabilities each time they successfully trade a security. ETFs rarely do so (other than dividends or interest) because internal ETF transactions are not viewed as taxable events. The only time an ETF investor can incur a capital gain tax liability is when they personally sell the ETF. Meanwhile mutual fund investors can incur a taxable distribution even in a year when the fund’s total return is actually negative. Unquestionably, ETF owners have superior control over the timing of their tax liabilities than those holding mutual funds.

Ned’s Notes Takeaway: Overall ETFs are cheaper, easier to trade and more tax efficient than mutual funds. However as there are nuances to these advantages, investors should be mindful that they must still must do their homework to decide which, if any, ETF is right for them.